- Offerings

- Tools & Platforms

Tools & Calculators

- Open API

- Calculators

- SIP Calculator

- CAGR Calculator

- Compound Interest Calculator

- FD Calculator

- RD Calculator

- EPF Calculator

- Retirement Calculator

- HDFC SIP Calculator

- Mutual Fund Return Calculator

- Lumpsum Calculator

- Step Up SIP Calculator

- ETF SIP Calculator

- Brokerage Calculator

- Equity Margin Calculator

- SWP Calculator

- EMI Calculator

- MTF Calculator

- Pricing

- SKY Learn

- Mutual Funds

- Margin Trading

- Financial Planning

- Personal Finance

- Share Trading

- IPO

- Derivatives

- Currencies

- Intraday Trading

- Trading Strategies

- Demat Account

- Commodity

- ETF

- What Are Long Term Capital Gains? Explained Simply

- How to Calculate Long Term Capital Gains on Shares: A Quick Guide

- Income Tax on Long Term Capital Gains in 2024: Everything You Should Know

- Exemption on Long Term Capital Gain Tax on Shares

- Handling Long Term Capital Loss: Smart Tax Management Move

- Comparison of LTCG and STCG Rates (2023-24 and 2024-25)

- Provisions for LTCG Disclosure in ITR Filing: A Complete Overview

- Conclusion: Simplifying LTCG Tax on Shares

- FAQs on Long Term Capital Gain Tax on Shares in India

- What Are Long Term Capital Gains? Explained Simply

- How to Calculate Long Term Capital Gains on Shares: A Quick Guide

- Income Tax on Long Term Capital Gains in 2024: Everything You Should Know

- Exemption on Long Term Capital Gain Tax on Shares

- Handling Long Term Capital Loss: Smart Tax Management Move

- Comparison of LTCG and STCG Rates (2023-24 and 2024-25)

- Provisions for LTCG Disclosure in ITR Filing: A Complete Overview

- Conclusion: Simplifying LTCG Tax on Shares

- FAQs on Long Term Capital Gain Tax on Shares in India

Long Term Capital Gain Tax on Shares in India and Exemption on Long Term Capital Gain Tax on Shares

By Ankur Chandra | Updated at: Jun 18, 2025 03:02 PM IST

According to Morgan Stanley, Indian households have earned an impressive $1 trillion from the stock market over the past decade. However, many investors were surprised to see a significant chunk of their profits go towards taxes. Understanding long term capital gains (LTCG) tax is not just about following the rules it’s about making smart investment choices and keeping more of your hard-earned money.

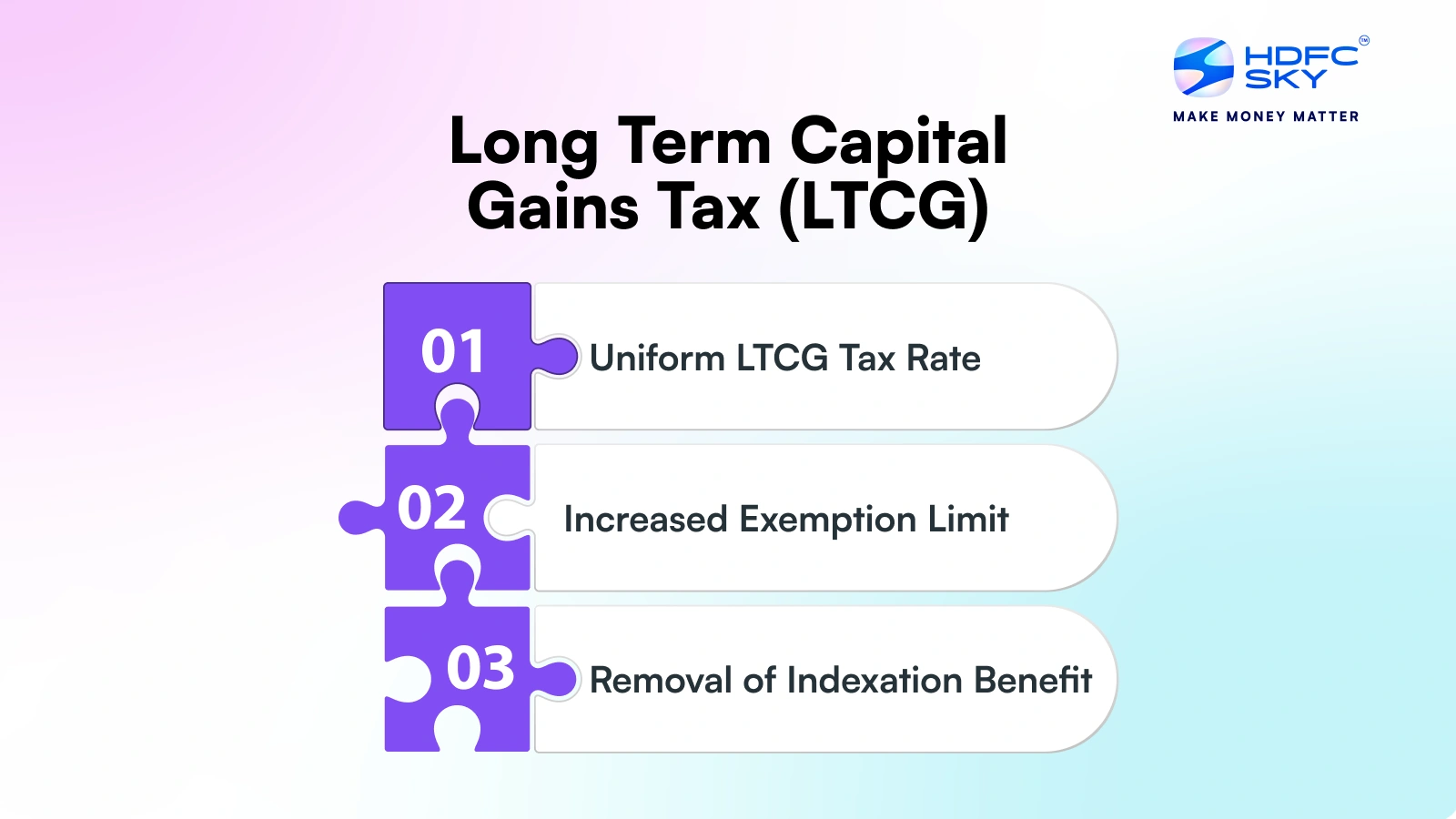

The recent Budget 2024 changes offer both opportunities and challenges. The increased tax exemption limit of ₹1.25 lakhs is a positive, but the higher tax rate of 12.5% underscores the importance of strategic investment planning.

Let us understand what is LTCG on shares and how to file long term capital gain tax on shares in income tax.

What Are Long Term Capital Gains? Explained Simply

Think of long term capital gains like the profit from selling a house you’ve owned for years. When you sell any valuable asset that you’ve held for a long time, the profit you make is called a capital gain. In the stock market, this concept applies to shares, but with specific rules about what counts as “long term.”

For shares and equity mutual funds, any holding period longer than 12 months qualifies as long term. If you bought shares of Company A on January 15, 2023, selling them on or after January 16, 2024, would result in tax on LTCG on shares.

This timing matters significantly because long term capital gain tax on shares in India are taxed differently – often more favourably – than short-term gains. It’s like getting rewarded for being a patient investor rather than a frequent trader.

How to Calculate Long Term Capital Gains on Shares: A Quick Guide

When selling shares, your final taxable gain is calculated by taking your total sale proceeds and subtracting all the costs involved in buying, maintaining, and selling those shares. Here is how long term capital gain tax on shares calculator works:

LTCG = Sale Price of Shares – (Cost of Acquisition + Transfer Expenses + Other Incidental Charges)

To find your taxable LTCG, begin with the amount you received from selling your shares. Then, you’ll need to subtract several important costs:

- First, deduct your initial investment – the price you paid when buying the shares. Think of this as your entry cost into the investment.

- Then, account for the costs involved in the actual sale transaction. These typically include your broker’s commission, transaction fees, and other charges you paid to complete the sale.

- Finally, factor in any additional expenses that were necessary for managing your investment, such as legal consultation fees or investment advisor charges.

Suppose you made the following share transaction:

- Sale Price (SP): ₹10,00,000

- Cost of Acquisition (CA): ₹6,00,000

- Transfer Expenses (TE): ₹10,000 (broker fees)

- Other Charges (OC): ₹5,000 (legal fees)

Plugging these numbers into our formula: LTCG = 10,00,000 – (6,00,000 + 10,000 + 5,000) = 10,00,000 – 6,15,000 = 3,85,000

This ₹3,85,000 represents your taxable long term capital gain. Under current tax laws, if this gain exceeds ₹1,25,000, the excess amount would be taxed at 12.5%.

In this case: Taxable amount = ₹3,85,000 – ₹1,25,000 = ₹2,60,000 Tax payable = ₹2,60,000 × 12.5% = ₹32,500

This formula ensures you account for all costs involved in your share transactions, giving you an accurate picture of your actual taxable gains.

Income Tax on Long Term Capital Gains in 2024: Everything You Should Know

Just as different roads have different speed limits, different types of gains have different tax rates. Let’s review the current tax structure that applies to your long term capital gains from shares in 2024.

For transactions happening after July 23, 2024, here’s how the tax system works:

- You enjoy a complete LTCG tax exemption on the first ₹1.25 lakhs of gains

- Beyond this threshold, a flat rate of 12.5% applies

- An additional surcharge applies if your total income exceeds certain limits

Exemption on Long Term Capital Gain Tax on Shares

While long term capital gains tax (LTCG) applies to profits from shares, certain exemptions can help you reduce your tax liability. Here are key exemptions available under the Income Tax Act:

- Section 54F: This section provides an exemption if the LTCG from shares is reinvested in purchasing or constructing a residential property within a specified time frame. To qualify:

- The entire sale proceeds must be reinvested.

- The reinvestment must be made within two years (for purchase) or three years (for construction).

- Section 54EC: If you invest your LTCG in specified bonds like those issued by the NHAI (National Highways Authority of India) or REC (Rural Electrification Corporation), you can claim an exemption of up to ₹50 lakh. The investment must be made within six months of the sale.

- Set-Off Against Losses: If you incurred long term capital losses in the same financial year or carried them forward from previous years, you could set them off against LTCG, reducing your taxable amount.

- Reinvestment in Equity Savings Scheme: Certain government-approved equity savings schemes may also provide tax benefits on reinvested LTCG.

- Threshold Exemption: Gains up to ₹1.25 lakh in a financial year are completely tax-free. This is particularly beneficial for small investors or those with limited gains.

Handling Long Term Capital Loss: Smart Tax Management Move

Sometimes, investments don’t go as planned, just like some recipes don’t turn out perfectly. However, losses can even have a silver lining in tax planning.

You incur a long term capital loss when you sell shares at a price lower than your purchase price after holding them for more than 12 months. These losses can be valuable because:

- You can offset them against other long term capital gains

- Any unused losses can be carried forward for up to 8 years

- These carried-forward losses can offset future long term capital gains

For example, You have two transactions in FY 2024-25:

- LTCG from Company A’s shares: ₹2,00,000

- Long term loss from Company B’s shares: ₹1,50,000

Your net taxable gain would be: ₹2,00,000 – ₹1,50,000 = ₹50,000

Since this is below the ₹1,25,000 exemption limit, you won’t pay any tax on these gains.

Comparison of LTCG and STCG Rates (2023-24 and 2024-25)

| Tax Rates for Listed Assets | ||||||

| Asset Type | Previous STCG Rate | Current STCG Rate | Holding Period (Months) | Change in Holding Period? | Previous LTCG Rate | Current LTCG Rate |

| Stocks | 15% | 20% | 12 | No | 10% | 12.50% |

| Equity Mutual Funds | 15% | 20% | 12 | No | 10% | 12.50% |

| Debt and Non-Equity Mutual Funds | Slab Rate | Slab Rate | N/A | Changed to STCG & LTCG same | Slab Rate | Slab Rate |

| Listed Bonds | Slab Rate | 20% | 12 | No | 10% | 12.50% |

| REITs/InVITs | 15% | 20% | 12* | Changed from 36 months | 10% | 12.50% |

| Equity FoFs | Slab Rate | 20% | N/A | Changed to STCG & LTCG same | Slab Rate | 12.50% |

| Gold/Silver ETFs | Slab Rate | 20% | 12 | No change | Slab Rate | 12.50% |

| Overseas FoFs | Slab Rate | Slab Rate | 24 | No change | Slab Rate | 12.50% |

| Gold Funds | Slab Rate | Slab Rate | 12 | No change | Slab Rate | 12.50% |

| Tax Rates for Unlisted Assets | ||||||

| Asset Type | Previous STCG Rate | Current STCG Rate | Holding Period (Months) | Change in Holding Period? | Previous LTCG Rate | Current LTCG Rate |

| Physical Real Estate | Slab Rate | Slab Rate | 24 | No | 20%** | 12.50% |

| Unlisted Bonds | Slab Rate | Slab Rate | 24 | Changed to STCG & LTCG same | Slab Rate | Slab Rate |

| Physical Gold | Slab Rate | Slab Rate | 24 | Changed from 36 months | 20%** | 12.50% |

| Unlisted Stocks | Slab Rate | Slab Rate | 24 | No | 20%** | 12.50% |

| Foreign Equities/Debt | Slab Rate | Slab Rate | 24 | No | 20%** | 12.50% |

Other notes:

- *Other than those investing 90% in equity ETFs

- **With indexation

- Those investing in funds with at least 65% equity

Provisions for LTCG Disclosure in ITR Filing: A Complete Overview

The Income Tax Return filing process for long term capital gains follows specific guidelines based on the taxpayer category and nature of gains. Here’s how different taxpayers should report their LTCG:

For Individual Investors and HUFs: Report long term capital gains from share transactions in Section B7 of ITR-2, unless these gains are business income. This applies when shares are held as investments rather than trading stock.

For Non-resident Investors: Different reporting requirements apply:

- Use Section B7 for ITR-2

- Use Section B8 for ITR-3

For Traders: If shares are treated as business inventory rather than investments, report profits under “Business Income” instead of capital gains. This typically applies to frequent traders rather than long term investors.

Remember to keep supporting documents handy:

- Demat account statements

- Contract notes for all transactions

- Bank statements showing fund transfers

- Computation sheets showing your calculations

Conclusion: Simplifying LTCG Tax on Shares

Understanding long term capital gains tax is like having a good map for your investment journey. It helps you plan better, save more, and stay compliant with tax laws. The recent changes in Budget 2024 have brought both challenges and opportunities – the increased exemption limit of ₹1.25 lakhs provides more room for tax-free gains, while the higher rate of 12.5% requires careful planning for larger profits.

Related Articles

FAQs on Long Term Capital Gain Tax on Shares in India

How to avoid long term capital gain tax on shares?

Minimise tax liability by strategically timing your share sales across financial years, utilising the annual exemption limit effectively. Consider selling portions in December and April to spread gains or explore tax-deferral through Section 54F by reinvesting in residential property.

What are the tax rules for long term capital gains?

Long term capital gains enjoy tax-free status up to ₹1.25 lakhs annually. Beyond this threshold, a 12.5% tax rate applies, plus applicable surcharges based on total income. Only the amount exceeding the exemption faces taxation. This system encourages long term investment while ensuring fair taxation on share trading and substantial gains.

What is the holding period for LTCG?

To qualify for long term capital gains treatment, investors must hold shares or equity mutual funds for 12 months plus one day from the purchase date. For example, if you purchase shares on March 15, 2023, the earliest date they qualify for LTCG treatment would be March 16, 2024.

What is the limit of LTCG tax free?

The current tax-free limit for long term capital gains from shares and equity mutual funds stands at ₹1.25 lakhs per financial year. This exemption acts as an incentive for long term investors, allowing them to earn substantial gains without any tax liability up to this threshold.

How to calculate long term capital gain tax on shares for filing return?

Calculating LTCG tax follows a systematic process. First, determine your total gain by subtracting the purchase price and any trading costs from the sale price. Then, apply the long term capital gain tax on shares exemption limit of ₹1.25 lakhs. If your total gain exceeds this limit, calculate 12.5% tax on the excess amount.